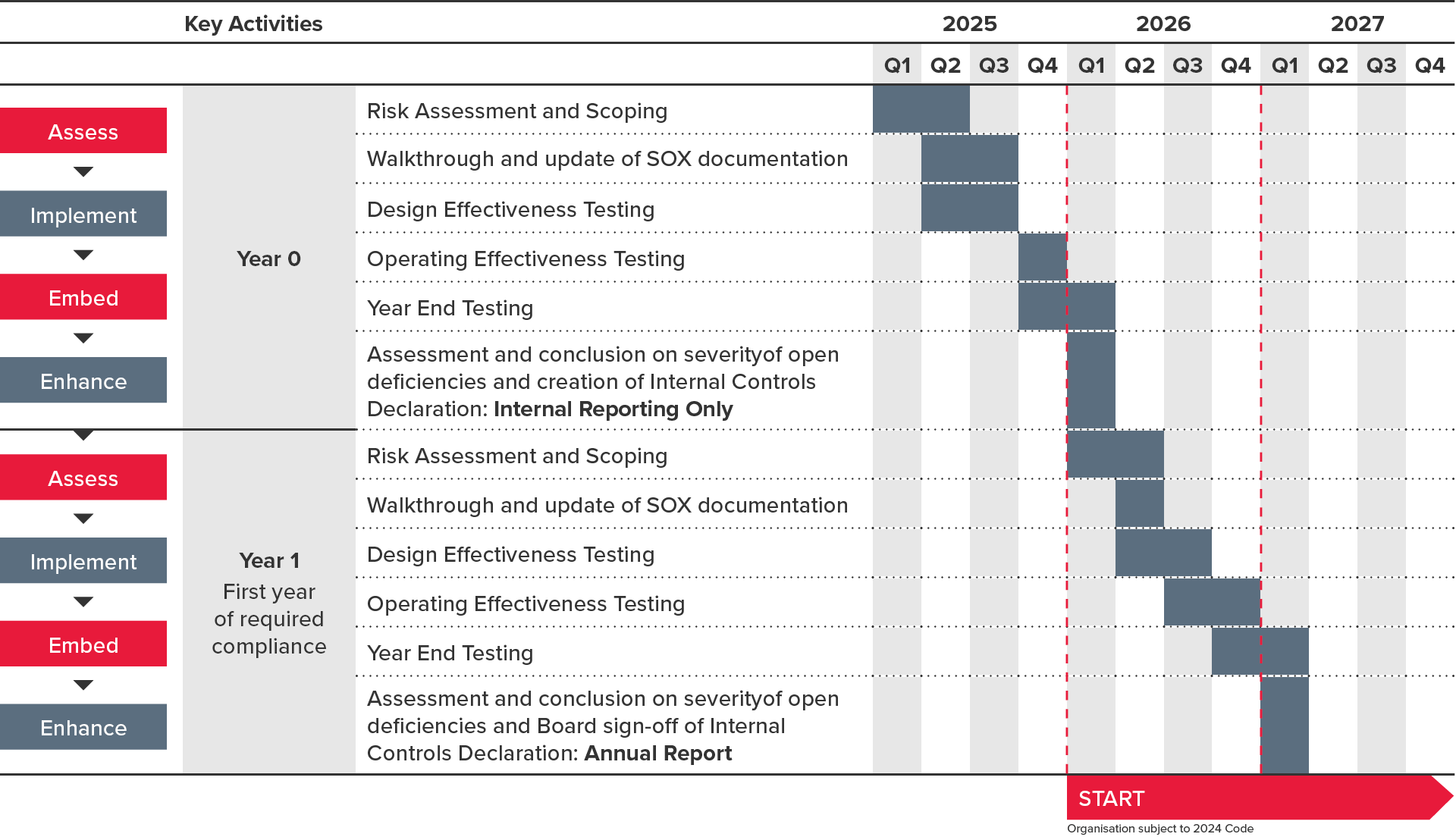

What is the Internal Controls Declaration?

The FRC has announced details of the New 2024 Corporate Governance Code, which creates the requirement for the board to make a public declaration an Internal Controls, this will require investment of time and resource to ensure compliance.

The changes will take effect for accounting periods beginning on or after 1st January 2026, so Boards will need to attest for years ending 31st December 2026 onwards. The declaration will be “as at” date and covers Operational, Compliance and Reporting (including Financial) controls and Boards will need to state how they have performed their monitoring of material controls in their annual report. Key elements that are required to be included in the annual report:

- A description of how the board has monitored and reviewed the effectiveness of the framework;

- A declaration of effectiveness of the material controls as at the balance sheet date; and

- A description of any material controls which have not operated effectively as at the balance sheet date, the action taken, or proposed, to improve them and any action taken to address previously reported issues

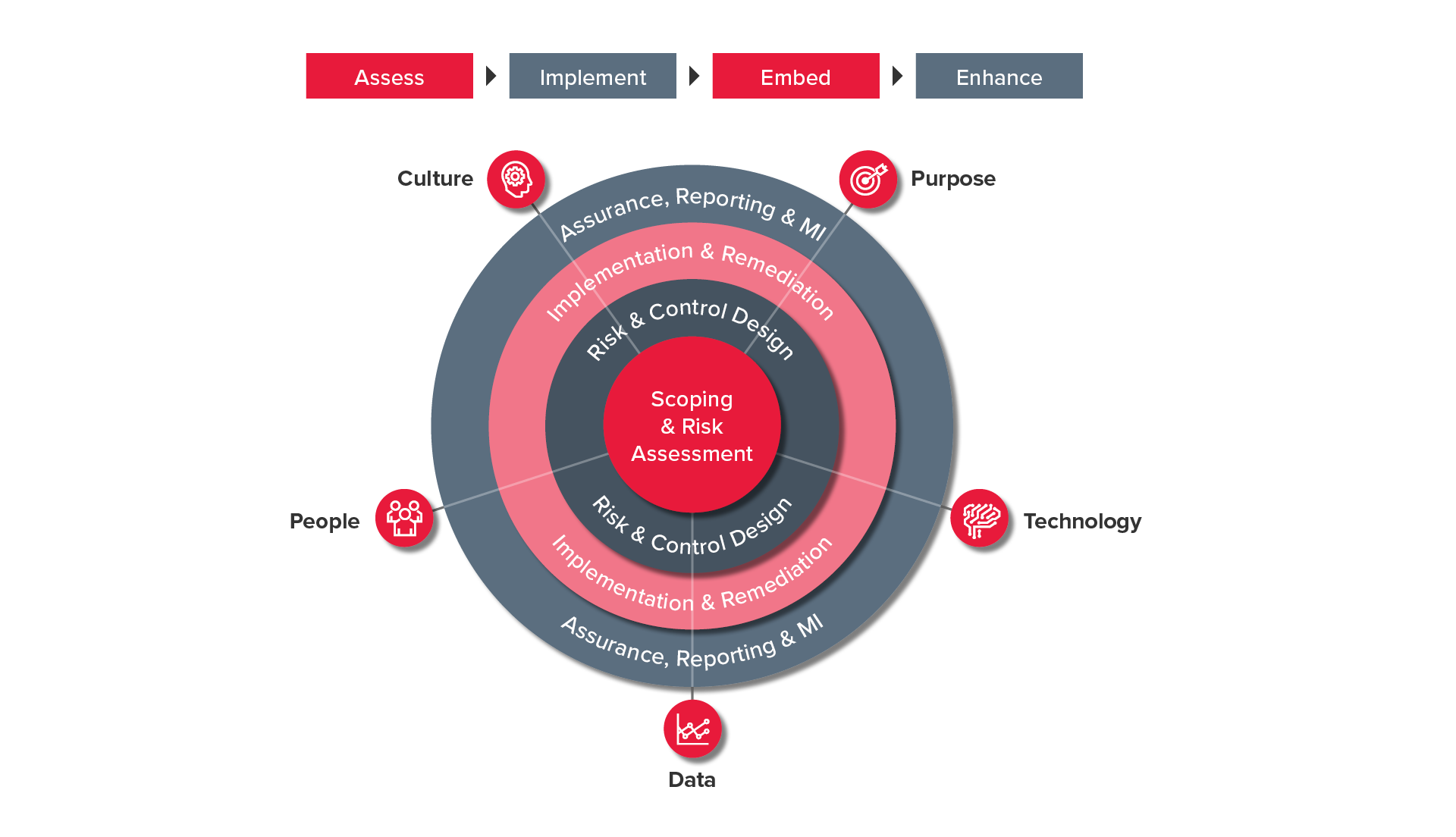

What is the value to the Board and C-Suite

Compliance with new requirements will require investment, while avoidance of penalties or sanctions is a driver, where is the real value?

Avoiding penalties and sanctions that will be part of the enforcement regime are an important drive, however directors, the board and management teams should also see the introduction of the Internal Controls Declaration as an opportunity to drive value and efficiency in their business.

- Improvements in the control environment, risk management and optimisation of assurance will drive increases in quality, efficiency and insight, through:

- Increased Executive Risk visibility with consistent measurement, metrics and leading indicators across the organisation – transition from a 'siloed reactive' to a 'consistent proactive' approach;

- Deeper control awareness and improved MI will enable greater transparency and accountability across the business – data analytics will drive deeper insight and shared learnings;

- Reduction in intensive manual activities and increased robustness and resilience of finance and IT functions.

- Almost 80 per cent of CFOs of US-listed companies said the overall quality of information in audited financial statements improved after SOx was introduced in the US1

- Energising the team and as a platform for improving ‘controls culture’ and driving the right behaviours across the organisation, especially with further changes on the horizon, such as the new ESG disclosure rules.

1. According to a poll by the Center for Audit Quality in 2017