Leaving the UK - breaking tax residence

Leaving the UK - breaking tax residence

There are many reasons why individuals decide to leave the UK; lifestyle, for work or other personal circumstances.

A move out of the UK can happen at short notice and you might intend your non-residence to have immediate effect. However, for tax purposes the date your residence begins, and ends is defined by the UK’s Statutory Residence Test (SRT).

You may wish to continue to spend time in the UK and remain non-UK tax resident. Once you have been UK tax resident, if you return to the UK after a period of non-UK residence there are additional specific matters related to your UK tax position to be aware of. These anti-avoidance rules have been widened in the 2025 Budget. It is best to understand the SRT rules so that you do not unintentionally become UK tax resident again.

Although it can be complicated, the SRT can provide more certainty surrounding the steps you must take to become non-UK resident, and remain non-UK resident, for UK tax purposes.

A new UK tax regime

A new income and capital gains tax regime was introduced from 6 April 2025 for new arrivers to the UK. New arrivers are individuals who have been non-UK resident for more than 10 years. This replaced the historic remittance basis of taxation in the UK. Read more about the changing rules for non-doms here.

The UK inheritance tax (IHT) rules also changed from 6 April 2025 to be based on an individual’s residence status. Now individuals who have been resident in the UK for more than 10 years will have a continued exposure to UK IHT on non-UK assets following departure from the UK. This exposure will depend on the length of time they were UK tax resident. Read more about IHT and protecting your family’s assets.

Statutory Residence Test

Your residence position in the UK is determined by the UK’s SRT. The SRT comprises three parts: an automatic overseas test, an automatic resident test and a sufficient ties test. The tests should be considered in that order and as soon as the conditions of one test are met, the other tests do not need to be considered.

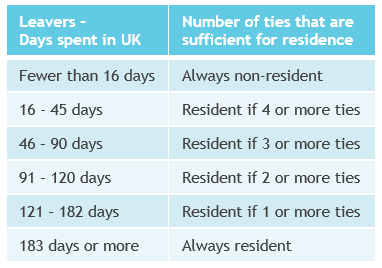

Under the ‘sufficient ties’ test your residence position can be determined by considering the number of connections, or ‘ties’, you have to the UK against the number of days you have spent in the UK in a tax year. You should keep detailed records to support your residence position. The more connections you have to the UK then the fewer number of days you may spend in the UK before you would be considered a UK resident. The connections that are relevant are work, family, accommodation, spending more than 90 days in the UK in the prior tax year and spending more time in the UK than any other country.

Click here for our practical guide to the Statutory Residency Test (SRT)

The guide provides an overview only and does not cover all the intricacies of the SRT. We always suggest getting personal tax advice based on your specific circumstances.