Reporting your corporate interest restriction

The CIR has a reporting regime that sits alongside companies’ CT600 filing obligations. The principle behind this is that the CIR operates at a group level even where a ‘group’ happens to consist of a single company.

It is important to note that filing a CIR return is separate from applying the CIR rules – those will remain applicable even if no filing is required. No company has an automatic obligation to prepare or file a CIR return, this only comes about if the group elects a reporting company or if HMRC appoints one for the group.

Two very different time limits exist for these different routes, and it is notable that it is only possible for a group to appoint a reporting company within 12 months of the end of the period of account. HMRC has a longer window, up to four years from the end of the period (or longer if relevant tax computations can be altered).

For periods ending on or after 31 March 2026, there will be more flexibility for timing as a return, without a separate 12-month time-limit for appointing a reporting company. There will, however, be penalties applied to any returns filed more than 12-months after the period end, or if it transpires the reporting company had not been appointed for the period.

When should a group appoint a reporting company?

All groups should first consider if they need to file a CIR return. Filing a CIR return is necessary in order to:

- Carry forward interest allowances

- Make certain elections under the CIR rules

- Allocate any interest disallowance to specific companies

- Allocate interest reactivations (which will not be relevant in the first period).

Where applicable, an abbreviated return gives a simple filing option that keeps flexibility to extend to a full return if beneficial.

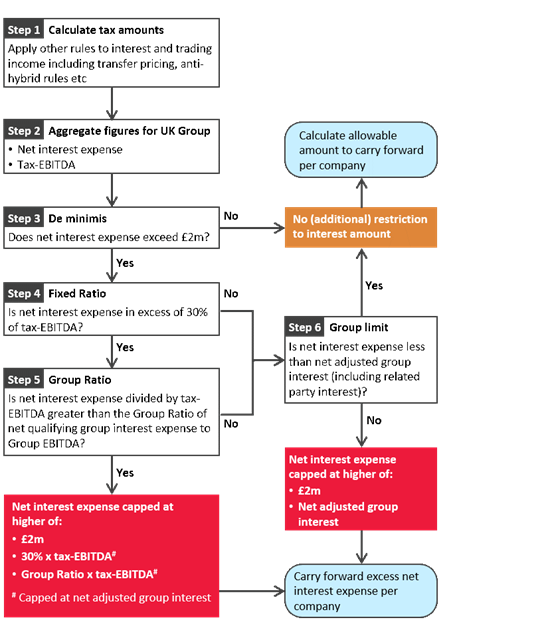

The CIR de minimis interest rules provides an important threshold when considering what approach to take. If the total net tax-interest expense across the UK companies in the group (i.e. tax deductible interest less taxable interest income) is below the £2m annual de minimis and won’t exceed this level in the next five years, there is unlikely to be any benefit in filing a return. In other cases, it is likely to be worth filing at least an abbreviated return.

What are the filing requirements?

Once a reporting company has been appointed, it will be obliged to notify the other group members of its status and to prepare a CIR return (until such time as the appointment is revoked by the group). The return will need be filed on the later of:

- 12 months from the end of the period of account (but see below for changes to groups)

- 3 months from the appointment of the reporting company (primarily where HMRC makes an appointment)

If a group has no interest restriction in a period, the reporting company can file an abbreviated return, which omits the detail of calculations but also does not allow interest reactivation or allowance carry forwards (unless/until replaced with a full return).

Returns must be filed through authorised software or through HMRC’s portal.

Late or amended returns can be filed up to 3 years after the period end.

Abbreviated returns

An abbreviated return may only be made if the group is not subject to a restriction of interest. It must contain:

- The name (and UTR if relevant) of the ultimate parent company of the group

- A list of the names and UTRs of all companies in the group

- A statement that there is no disallowance

- A statement that the return is accurate.

Full returns

A full return must contain the same detail as abbreviated return, plus:

- A statement of calculations, including details of tax-interest and tax-EBITDA figures for all companies subject to UK tax, relevant accounts-based figures and the interest allowance and interest capacity

- Statement as to whether there is a disallowance and if so detail on how it is allocated

- Statement as to whether there is a reactivation of interest and if so detail on how it is allocated.

Appointing of a reporting company

Once you (or HMRC) have decided that returns are appropriate, a ‘reporting company’ needs to be appointed by a majority of eligible companies in the group (i.e. those in the charge to UK corporation tax and not dormant throughout the period).

This must generally be within 12 months of the period end for which a return is appropriate. If you have missed the deadline, it is possible to ask HMRC to appoint a company for the group. In the 2025 Budget it was announced that HMRC has revised its policy. The CIR rules are now being amended for periods ending on or after 31 March 2026 so that groups will appoint a reporting company without notification to HMRC, in line with rules for administering group loss relief, with a new requirement for the appointment to be made for each period (ie with no carry forward).

As noted above for filing returns, for periods ending before 31 March 2026, the appointment of a reporting company must be made through approved software or through HMRC’s online portal.

The reporting company must notify the eligible companies (and the ultimate parent company) that it has been appointed. The reporting company will be granted statutory powers to require the relevant data to complete a return from other UK group companies.

It is worth remembering that if some group members, or companies that have left the group during the period, do not wish to be bound by the reporting company, it is possible for them to elect to be ‘non-consenting companies’. This status limits the potential allocations of disallowances to the affected companies and may be relevant in groups with diverse management teams or minority shareholders.

An appointment may be revoked by a majority of eligible companies.

Potential pitfalls

Areas that could catch groups out include:

- A group is defined based on the holding company – therefore a company can be part of several groups during an accounting period and if a new holding company is inserted it is likely that an entirely new group would be formed. As the reporting deadlines usually run from the date first group ‘ends’, it is important that appointment of reporting companies should be considered for each relevant ‘group’ during the accounting period.

- Final figures might not be considered across the group until it is too late to appoint a reporting company for the period, especially if significant tax adjustments could be required.

- Certain delayed interest amounts, such as late paid interest or interest capitalised into the cost of stock, may make a return or elections beneficial when there would not appear to be disallowances.

- The group may have a period distinct from some or all UK group companies, complicating calculations (with CIR deadlines based on the group’s period), and multiple dates may need to be considered where there are multiple groups.

- The £2m annual de minimis is pro-rated for short periods.

If there is any doubt over the benefit or importance of a CIR return, it is prudent to appoint a reporting company for the group within the deadline.