Employee Ownership Trusts (EOT)

Employee Ownership Trusts (EOT)

The tax-advantaged sale of a business to an employee ownership trust (EOT) has continued to attract business owners seeking an exit and its increasing use has resulted in significant growth in the number of employee-owned businesses in the UK. While achieving the Government’s original objectives, the wider use of EOTs has led to the Government expanding the number of qualifying conditions to eight in Budget 2024 and reducing the CGT relief on the sale from 100% to 50% in Budget 2025 to limit the predicted future cost to the Exchequer.

Since the inception of EOTs in September 2014, selling your company to the corporate trustee of an EOT has increasingly appealed to shareholders when dealing with succession planning issues. It is estimated that there are now approximately 2,500 companies which have been acquired by the trustees of EOTs across all sectors and sizes, with a current run rate of 500 companies per year becoming employee-owned.

In our experience, selling your company to an EOT has recently been the fastest growing exit mechanism for small and medium-sized companies - many shareholders are now seeing a sale to an EOT as a direct alternative to a standard trade sale or a management buyout. However, whether this trend continues is now up for debate following the 2024 and 2025 Budgets which first tightened the rules and then subsequently cut the relief. We are of the view that, after the 2024 and 2025 Budgets, sales to EOTs still create great opportunities for shareholders to sell their companies to their employees efficiently and cost-effectively, for their full commercial market value, and in one of the most tax-efficient ways possible.

What is an EOT?

An EOT is a special form of employee benefit trust introduced in 2014 to encourage more shareholders to set up a corporate structure like the John Lewis model. The aim is to facilitate wider employee-ownership, via an indirect holding.

The Government introduced very generous tax breaks to encourage shareholders to move to an employee-ownership model. However, to qualify for the tax incentives, the employee ownership needs to be structured in a particular way.

EOTs are not just an option for traditional companies. Limited Liability Partnerships and companies that are part of a bigger group can also adopt an employee ownership structure. It is possible to find commercial and innovative ways to transition almost any type of business to employee ownership structures.

What's new?

The Government announced that the statutory capital gains tax relief available to UK shareholders on disposals to Employee Ownership Trusts (EOTs) will be reduced to 50%, with effect from 26 November 2025.

The combined impact of a very challenging M&A market, global instability and low economic growth has resulted in a substantial spike in the number of shareholders looking to sell their companies to Employee Ownership Trusts.

The total number of UK employee owned (EO) businesses towards the middle of 2025 was c.2,500, with a total of 560 new EO business in 2024.

This should continue, largely unaffected by the 2025 changes, primarily because the tax relief is just one of the factors in many business owners’ decisions to transition to employee ownership and a 12% rate of tax on a sale to an EOT is still one of the most tax-efficient transactions available for UK shareholders.

Why choose to sell to an Employee Ownership Trust?

UK resident shareholders are able to sell shares in their company for a full commercial market value and claim a complete UK Capital Gain Tax exemption, subject to satisfying certain statutory conditions.

Employees can receive:

(i) annual tax-free cash bonuses of up to £3,600 per employee per year, and

(ii) share-based incentive awards.

One of the most important benefits of being an EO business is that employees have a stake in their company and the greater employee engagement and commitment that results from this.

Many companies have also found that moving to an EO model has been a “game changer” for their ability to attract and retain key talent.

If you are looking to sell, there are numerous reasons why you might choose to sell to an EOT rather than a standard trade sale. These include:

(i) allowing shareholders and directors to conclude a quick and smooth transition of the company to the employees via an EOT, allowing management to focus on running the business rather than being embroiled in time-consuming sale negotiations;

(ii) allowing shareholders to receive full value for their business without the need for earn-outs - a proportion of earn-outs never pay out to the extent expected by shareholders;

(iii) using the power of employee-ownership to engage and motivate your workforce to take the company to the next level;

(iv) substantially lower transaction fees; and

(v) allowing UK shareholders to claim a 50% UK capital gains tax exemption on the disposal.

If you own a trading company, you can now sell some, or all, of your shares to an employee ownership trust (subject to satisfying certain conditions) for full market value at a advantageous capital gains tax rate in a way that also benefits your employees.

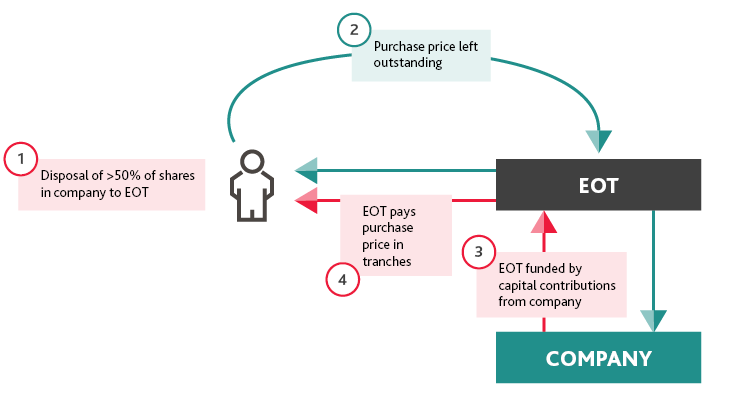

How does a sale to an EOT work?

There are three key steps in selling a business to an Employee Ownership Trust:

- Establish a qualifying EOT with a UK resident corporate as the trustee of the EOT (the Trustee Company).

- The shareholders will sell their shares to the Trustee Company under a share purchase agreement. The shareholders and the Trustee Company should jointly engage a share valuation expert to value the company: the Trustee Company will use this value as the basis for determining the purchase price. On the sale of the shares, the purchase price will create a debt owed by the Trustee Company to the shareholders, which will be left outstanding (see diagram).

- The company will continue to generate trading profits each year and it will use these profits to make distributions to the EOT. The EOT will use these distributions to repay the outstanding purchase price that it owes to the shareholders.

What are the advantages of selling to an EOT?

There are many advantages for shareholders:

- It allows employees to indirectly buy the company from its shareholders without them having to use their own funds - thereby creating an immediate purchaser and addressing any succession issues.

- Shareholders can sell their shares for full market value after an independent valuation. The Trustee Company must take all reasonable steps to ensure that the consideration for the disposal does not exceed the market value of the ordinary share capital at the time of the disposal, and where part of the consideration for the disposal is deferred, that the rate of any interest payable on the deferred consideration does not exceed a reasonable commercial rate.

- No income or inheritance tax liabilities should arise on the disposal of a controlling interest in a company to an EOT, or on the subsequent receipt of the purchase price by the former shareholders.

- Any gain realised is 50% exempt from capital gains tax, giving an effective rate of 12% - no Business Asset Disposal Relief is available on the disposal.

- Not all shareholders are required to sell their shares to the EOT.

- The directors can remain in situ post-disposal, and can continue to receive market-competitive remuneration packages.

- The EOT is generally seen as a “friendlier purchaser”, which means the sale process may be quicker, with potentially lower fees.

What are the advantages for the company and employees?

As all employees get an indirect stake in the company, there are substantial practical benefits associated with being owned by an EOT:

- Greater employee engagement and commitment

- Reduced absenteeism

- Greater drive for innovation

- Improved business performance.

Companies controlled by EOTs can also pay tax-free cash bonuses to their employees of up to £3,600 per employee per year – these payments are still liable to National Insurance.

Key qualifying conditions

To carry out a qualified sale to an EOT there are eight key conditions to meet:

- The company whose shares are transferred must be a trading company or the principal company of a trading group.

- The trustees of the EOT must restrict the application of any settled property (the shares) for the benefit of all eligible employees on the “same terms”.

- At least 50% of EOT trustees (and persons “connected” to them) must not be “excluded participators”; and the company must not be under the “control” of excluded participators. If a corporate trustee is used, the majority of the directors of that trustee must also not be “excluded participators”. An “excluded participator” is a shareholder or former shareholder of the company but does not include someone who was not beneficially entitled to, or to rights entitling them to, acquire 5% or more of, or of any class of, the shares comprised in the company’s share capital; and on a winding-up of the company would not be entitled to 5% or more of its assets.

- The trustees must be UK resident and retain, on an ongoing basis, at least a 51% controlling interest in the company.

- The number of continuing shareholders (and any other 5% participators) who are directors or employees (and any persons connected with such employees or directors) must not exceed 40% of the total number of employees of the company or group.

- Trust property must generally be applied for the benefit of all eligible employees on the same terms but the trustees may distinguish between employees based on remuneration, length of service and hours worked.

- The trustees must take all reasonable steps to ensure that both (i) the consideration for the disposal does not exceed the market value of the ordinary shares; and (ii) if interest is charged on deferred consideration, the rate of interest does not exceed a reasonable commercial rate.

- The individual must not have made a claim for CGT relief under these provisions for a previous disposal of ordinary shares in the target company.

Your next steps

Our team is the market leader in advising on transactions with EOTs and employee-ownership and can provide you with free, practical and user-friendly advice on the advantages and disadvantages of selling your business to an EOT.

In just the last year, we have worked with numerous companies, as well as LLPs and groups, on establishing employee ownership structures via Employee Ownership Trusts. They have ranged from companies with just 10 employees to over 1800, with enterprise values from £3m to over £750m and from all sectors. We are helping shareholders sell their businesses while navigating the many pitfalls that can catch-out the unwary.

For help and advice on selling your business to an Employee Ownership Trust please contact Matthew Emms.

Recent client testimonials

- “Simply 10 out of 10 in all areas. We turned to BDO for advice because we trusted that they would be accurate, timely, pragmatic and responsive. They exceeded our very high expectations. Matthew was excellent technically and a pleasure to work with."

Ben Tolley, Finance Director, Clarity Capital Partners Limited - “The shareholders decided that if we were going to transition the business to an Employee Ownership Trust, we wanted best in class advisers and that's what we got. Working with Matthew and his team (particularly Andrea) has been an exceptional experience. Matthew brought not only deep technical expertise in EOT structuring, tax and accounting, but also a calm, pragmatic approach that helped us navigate what was for us was a complex process with confidence. We didn’t always agree but his ability to distil intricate legal and financial concepts into clear, actionable advice was invaluable - particularly when aligning our goals with HMRC requirements and helping us and the lawyers manage the complex FCA change of control process. One of my early concerns was cost - specifically whether the final bill would exceed the original quote. I needn’t have worried, all costs were exactly in line with what had been agreed with Matthew nearly six months before completion. Matthew’s collaborative style, responsiveness, and genuine commitment to our continued success made him feel like an extension of our team. His guidance was instrumental in shaping a structure that preserves Clarity’s independence, rewards our people, and secures our long-term legacy. I would not hesitate to recommend Matthew and his team to any business considering an EOT- he has become a trusted adviser in every sense.”

Craig Gibson, Commercial Director, Clarity Ltd - “Every aspect of my dealings with BDO and, in particular, with Matthew Emms was outstanding. He had a great way of making a complicated process sound very simple. He is always available, and it is never an issue talking to him. He could never do enough for us. Chris Barker was also absolutely superb. You could always get hold of him. He dealt with everybody in a polite and caring way so that people weren’t nervous about asking questions. Every way they communicated with us they fulfilled what they said they were going to do.”

Kevin Greenyer, Finance Director, GBE Group - “The EOT team at BDO were exceptional. Their encyclopaedic knowledge of the scheme coupled with their foresight into the likely future direction it will take was second to none. There isn't another team on earth I'd have rather had helping us through to completion.”

Ian Witts, QuickThink Cloud Ltd - “I have recently worked with Matthew / BDO and I only have high praise for them. They have navigated me through a complex shareholding structure with real expertise, a down-to-earth approach, a high level of flexibility, impressive responsiveness and a much needed sense of humour. Couldn’t fault them.”

Caroline Kinsey, Chairman and owner of Kinsey PR Limited